The ECB’s Greek Bond Holdings and what the ECB could do

Every time I mention that the ECB could convert their holdings to PSI bonds, I’m told it wouldn’t make a difference. Well, currently I see €56.6 billion of bonds that are specifically labeled as series “CBE” or are Greek law bonds that would have PSI’d otherwise. It seems a bit larger than some other numbers as some EFSF bonds or holdings are included.

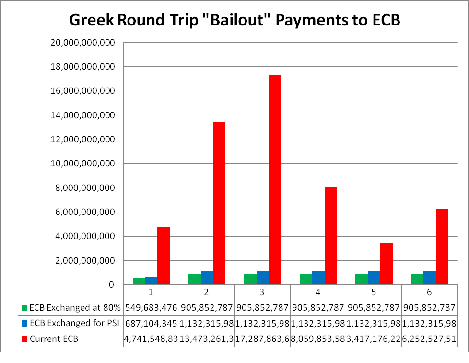

I am not saying the ECB should go through PSI, just that if they converted all of their bonds to the 2023 PSI bond at cost, the bailout package would have to be much smaller. If they actually converted them at 80% to reflect an estimate of cost, the savings is even greater. I calculate that Greece will spend about €53 billion servicing the ECB’s SMP holdings between now and the end of 2017.

Just exchanging for €56.6 billion of PSI bonds would save Greece almost €47 billion over that time period.

Other than the fact that the ECB has promised to pay the profits to other central banks, I can’t see what the true cost is. In the real world, where the ECB didn’t effectively control their own cost of funds, there would be a cost, but for the ECB?

Rumors that the Spanish bank bailout will involve long maturity low coupon bonds would be an indication that the EU understands how important that can be in making a plan feasible. Even today, rumors of Ireland getting their deadlines extended made the circuit.

Greece is a very tricky situation, but it is clear that the bailout, as structured doesn’t work. Germany doesn’t want to back of the austerity (much), but if they aren’t careful, they will see the cost of all their frivalous guarantees and backstops come back to haunt them quicker than they ever thought.

Letting the ECB do more may be more politically acceptable, and seems that taking a “voluntary” extension is less likely to harm the ECB’s future ability to help in Europe than being hit with involuntary defaults. But then again, Merkel and the rest of the EU have managed to screw up every stage of this crisis. I continue to believe Europe would be in far better shape now had they let Greece default back in 2010, but now after years of guarantees and quasi-integration, they are less prepared for a Greek default than ever.

The one thing I know for certain, is I should have gone to Mexico since that’s where all the rumors are, and I have to believe it would be more fun waiting for the next one to hit while there, than being here, especially if the heat wave turns out as bad as they project.