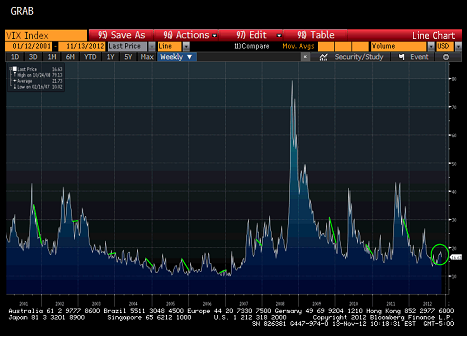

Vix – Seasonality may be making VIX look more complacent than it is

I’m hearing lots of concerns that VIX is low so the selling isn’t over. It is definitely lower than it was pre-election, but that makes sense as a big one time outcome was taken off the table but could be a sign that there is complacency. It is still higher than where it was post OMT and QE, so maybe there is still some fear in the market.

The one thing that is ignored in that, is it seems that November to December is generally a low period for VIX. The chart isn’t great, and isn’t always showing a decline, but it does seem to highlight that VIX has seasonality. That makes sense to me.

VIX is a calculation based on the average volatility that investors are willing to pay for an option. There is a core group of players who continue to play “gamma” in the options. There are those who look at the daily “decay” in option premium. Those investors will pay less because there are fewer trading days, and some of the days that are trading days are thinly staffed and tend to be directionless sessions.

So be careful reading too much into a VIX that is low, without trying to account for the seasonality. In fact we might have more fear priced in that is obvious.

The other big “fear” tell is the CDX basis. It is less well followed, so it might actually be useful. IG19 is trading a touch cheap to intrinsics. IG18 traded cheap a few times and it was usually right near the end of a widening move. It hasn’t been a perfect signal (otherwise it wouldn’t exist), but has been decent.

I think sentiment is far less positive and far more bearish than people believe, and while not at the levels we saw in the summer, is meaningful. Being long risk feels dangerous here, and I do think that a big move is more likely to be to the downside than upside, but that a gradual move higher is the most likely outcome in the near future.