The T-Report: Spain, Italy, & HYG. All driving markets lower

Spain and Italy. Spanish 10 year yields are heading to 6%. They are at 5.94% and without some ECB intervention soon are likely to pierce 6%. I think we are on the cusp of a lot of stop loss orders and with limited liquidity, the move could be fast and painful. We remain with a Spanish 10 year short on our “best ideas” list, and changed S&P long to short earlier this morning based on the weakness in Spain and Italy.

Not only is the 10 year bad, but you are seeing a “bear flattening” across the curves as the shorter dated bonds underperform on a yield basis. Spanish 5 year bonds finally trade on top of each other, but with 5 year CDS 45 bps apart (480 for Spain and 435 for Italy) that trade still has room to run.

Don’t be fooled by the initial strength in US Futures. It was as much a function of European investors switching out of shorts there that they put on with European markets closed, as it was anything to do with positive news out of the U.S.

The NFP data continues to be dissected, and it seems that more people are arguing the weather affect actually helped the March data. The belief in some circles (including this one) is that March’s great weather kept the jobs number higher than it would have been otherwise. The real payback is yet to come, and there is virtually no evidence that the hiring in December, January, and February led to any real permanent uptick in economic growth.

Alcoa comes out tonight. Is there any chance that we go through a period of moderate economic growth and moderate earnings weakness? That is my view. Look for some weakness in stocks as a direct result of earnings.

Maybe the markets have declined too far, too fast, but I think the bounce yesterday afternoon (prior to the late day fade) and the overnight bounce are all we are going to get. That took out some shorts, and let a few buy the dip people spend their money. They need to be nervous, and the real “too far too fast move” was the big move higher. I am looking for S&P to break the 50 DMA today before thinking about covering this short. If anything tempted to add more shorts – either S&P, IG18, or Italian CDS.

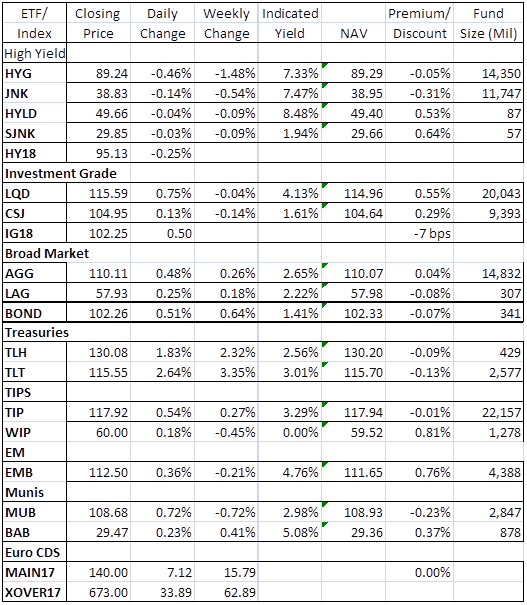

HYG in particular got hit late day. That and JNK both trade at a discount now. There are some rumors that the other side of the “whale” trade is shorts in high yield. That would explain some of the almost inexplicable weakness in the “compression” trade. HY CDS has been underperforming IG CDS in what was a tightening market – which was very strange to say the least.

The discount to NAV for the HY ETF’s is important to watch. We need to see how real it is. It might just reflect that NAV didn’t adjust to weakness in the underlying market. That is okay. If the discount is real and can be arbitraged, then watch out. We could see selling pressure on the bonds in the ETF’s (which also happen to be the bonds most hedge funds hold) and see a wave of share redemptions as the arb trade goes the other direction (the premium was, as paradoxical as it might seem, a key driver in share creation).